Academic pharmacist Nataly Martini highlights the importance of understanding non-Hodgkin lymphoma and pharmacists’ roles in managing this condition

Friday 1 November 2024, 01:00 AM

14 minutes to Read

Website intended for a NZ health professional readership

We are on our summer break and the editorial office is closed until 17 January. In the meantime, please enjoy our Summer Hiatus series, an eclectic mix from our news and clinical archives and articles from The Conversation throughout the year. In April, Jonathan Chilton-Towle investigated the sustainability of the sector, identifying the pressure points and opportunities

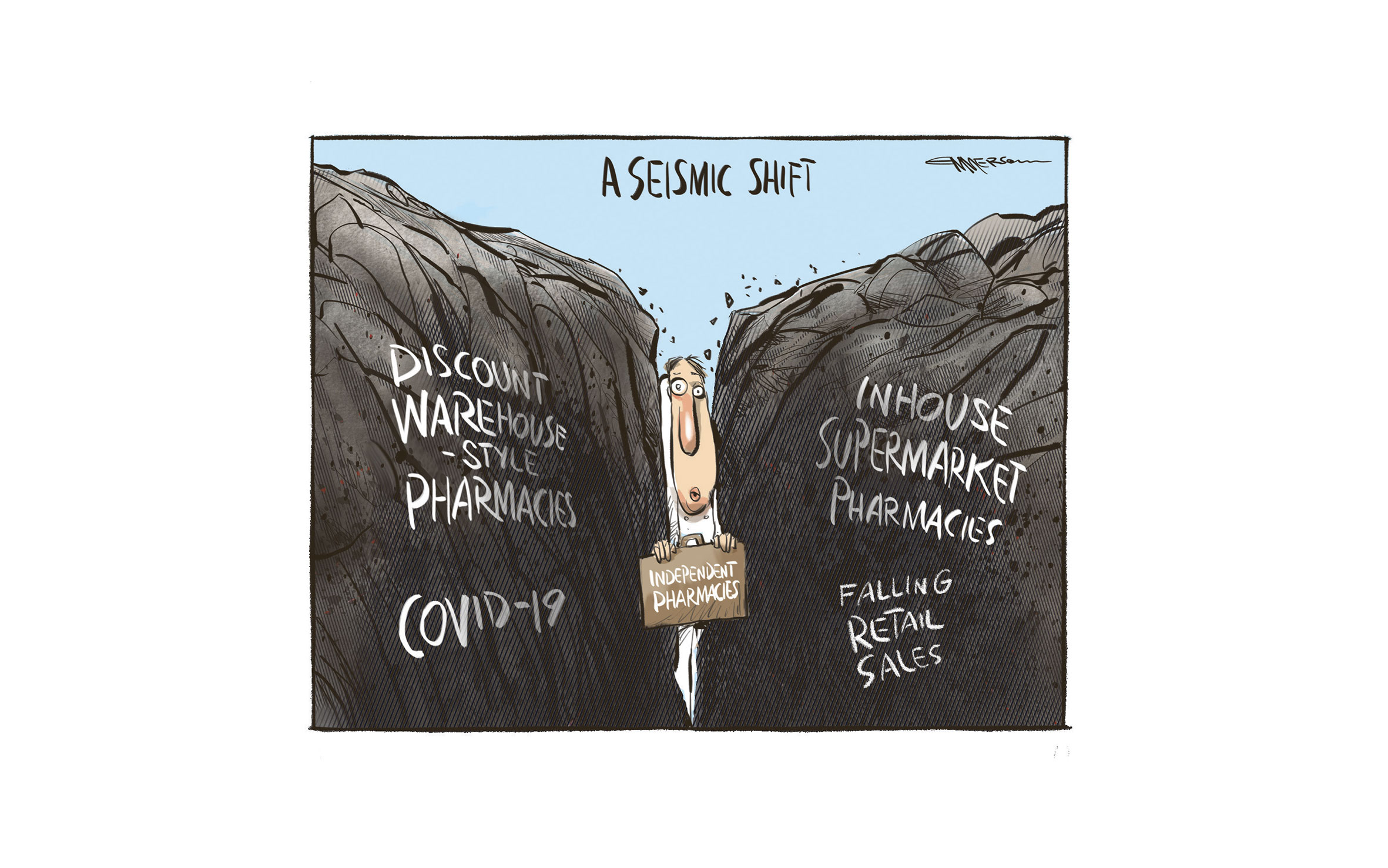

Numerous pharmacy closures have been predicted ever since the opening of the first Chemist Warehouse in October 2017 and the introduction of the evergreen Integrated Community Pharmacy Services Agreement the following year.

Three years on, more pharmacies are closing but that number is eclipsed by new businesses opening, despite widespread concerns about the financial sustainability of the sector.

Figures from the Ministry of Health show that from July 2018 to now, 69 pharmacies have closed across the country, while 97 new pharmacies have opened.

The rate of closures does seem to have stepped up in the past two years. Between July and December 2018, just five pharmacies closed nationwide. Thirty-one pharmacies closed in both 2019 and 2020 but in both years more opened, 37 in 2019 and 33 in 2020.

So far in 2021, two pharmacies have closed and two have opened.

Broken down by DHB regions, it is clear most of the action is happening in Auckland and Canterbury, the areas most affected by competition from discounters. In Canterbury, nine pharmacies closed and 18 opened during this period. And in Auckland, 33 closed and 43 opened.

69 pharmacies closed since July 2018

The Auckland district was the only large DHB area where the number of pharmacies that closed was slightly more than the number that opened in both 2019 and 2020.

Jonathan Roberts, Auckland director at the accountancy firm Moore Markhams, says most of the new pharmacies he is aware of opening now are large ones, either discounters such as Chemist Warehouse and Countdown, or other large corporates, often at purpose-built medical centre sites.

This observation is true for the Ormiston Kiwi Chemist, a new 100sqm pharmacy that opened last month in a brand-new, purpose-built 3000sqm medical centre in the Auckland suburb of Flatbush.

Owner Michael Mishriki believes selecting a good location is key to running a successful pharmacy in the current climate.

“You just have to be a bit more discerning with the pharmacies you open or buy.”

For instance, the medical hub housing his pharmacy includes six doctors, a dentist, a physio and a radiologist so it should have a good volume of prescriptions in addition to its retail.

The pharmacy is Mr Mishriki’s fifth, and he is not discounting prescription fees in an attempt to compete with discounters at any of them.

He believes independents can still compete, if they do everything they can to look after their patient base.

Meanwhile, the pharmacies closing are smaller independents and Mr Roberts believes more will close in the near future, although he always advises owners to consider a merger before liquidation.

The most recent Moore Markhams benchmarking survey released in December identified that pharmacies with revenue of less than $1 million, returned on average a net profit percentage of only 1.3 per cent which calls into question the viability of the business.

The survey found 27 (or 17.5 per cent) of the 154 pharmacies surveyed, fell into this category and 18 of these pharmacies were in the Auckland.

Mr Roberts believes this is a fair representation of the New Zealand pharmacy sector, so extrapolating that figure to the total number of independent pharmacies, there might be around 157 pharmacies in the same position nationwide.

Several pharmacy sector experts have pointed out that location is a major factor in pharmacy viability, especially since COVID-19 reduced foot traffic in malls and city centres.

In April last year, Wellington-based pharmacy accountant Hugh Lopdell, of Oak Park Chartered Accountants, described the impact of the pandemic as a “tale of two cities” with central city pharmacies seeing the biggest drop in revenue and suburban pharmacies being less affected.

John Saywell, chief executive at retail consultancy firm RPM Retail, has also noticed this trend. Mr Saywell says some pharmacies are no longer viable and believes there will be a drop in overall numbers, although he cannot say how many will close or how fast it will happen.

“Some smaller pharmacies will close because they can’t afford to grow their services or retail. Some big ones in poor locations will also close.”

Falls in retail revenue, which is intended to subsidise the dispensing business in the pharmacy funding model, have also had a massive impact on pharmacy viability, and this started long before discounters arrived on our shores.

Mr Saywell says pharmacy retail profits have been declining for at least the past 20 years due to competition from other retailers moving into areas, such as beauty products, that were traditionally the domain of pharmacy.

The beauty category is now down an estimated 75 per cent and many pharmacies have exited altogether, he says.

Natural products sales have replaced the loss, but now discounters are going for that market and Mr Saywell predicts losses here will “hurt”.

Until recently, the decline in retail sales was 1 or 2 per cent per year but the decline has doubled in the past 12 months (the past 18 for Auckland).

Some smaller pharmacies will close because they can’t afford to grow their services or retail. Some big ones in poor locations will also close

The decline was caused not only by competition from discounters and attrition of products to other channels, but also by some surprises caused by COVID-19, such as customers not returning to central business districts (CBDs) even after the lockdowns finished, and a lack of tourists.

“CBDs and shopping malls are no longer the place to be. Some smaller suburban locations have benefited.”

Pharmacy Guild chief executive Andrew Gaudin says it has reached the point where a discussion is needed on whether it is still worthwhile for pharmacy services to be cross-subsidised by retail.

“We are seeing a reduction in returns for pharmacy owners to such an extent that for some people it’s actually questionable whether it’s worthwhile to be in business,” Mr Gaudin says.

It is hard to quantify the scale of losses, but Mr Gaudin says the guild worked out most pharmacies operated at a loss during lockdowns, and gave that advice to the ministry and DHBs. That led to the creation of the $18 million pharmacy relief package from the Government.

As of the end of February, only around $430,000 of this money has been paid out and Mr Gaudin says the guild is advocating for the rest to be split between all pharmacy owners rather than the current targeted approach.

Retail losses are a significant factor in pharmacy viability, but there are other contributors too, including the underlying funding system not providing enough money to cover the cost of service delivery and business overheads.

For some frequently repeated medicines, the guild believes margins paid to pharmacies might be below the actual cost of delivering the services. Additionally, pharmacies are dealing with increased costs caused by out-of-stock medicines and extra workload from moving to virtual service, Mr Gaudin says.

The Moore Markhams 2020 benchmarking survey shows dispensary activities make up 75.8 per cent of the average pharmacy’s income, compared with retail, which makes up 24.2 per cent.

Even 10 years ago, we could do it because retail was good but now we can’t compete with larger retailers and their loss leaders

The average pharmacy dispensed more than 74,000 scripts last year and on average made $22.13 on each.

This is an increase from $21.48 in 2019 and $19.54 in 2015, but the survey notes that the increase in average dollar value per dispensing indicates drug costs are rising.

Overall, the clear trend is that pharmacy revenues are shrinking. Last year’s survey was the first, since the surveys started in 2013, to record an average pharmacy net profit higher than the previous year. This was due to an abnormally busy March when customers were panic buying before the first lockdown.

The survey shows the average pharmacy net profit before tax was 5.9 per cent of revenue in 2020, compared with 8.5 per cent in 2013.

The three key drivers affecting pharmacy sustainability, according to Mr Gaudin, are discounters reducing script and retail volume, COVID-19 reducing revenue further, increasing operating costs such as new safety measures, and hospital deficits meaning DHBs have little money left to spend on pharmacy.

HeeSeung Lee, owner of three pharmacies in Auckland, says increases for dispensing and service fees are far below rises in cost of business overheads.

“Dispensing [payments] doesn’t go up with the Consumer Price Index. But every year our operating costs increase with CPI at a minimum,” Dr Lee says.

That combined with intense commercial competition and a drop in customers caused by COVID-19, has left pharmacies throughout the Auckland region living “hand to mouth”.

She believes many owners will be footing the bills themselves, dipping into already small profits, business loans and even credit cards.

“Even 10 years ago, we could do it because retail was good but now we can’t compete with larger retailers and their loss leaders.”

Mr Gaudin says the single biggest unmet cost pressure is wages.

According to last year’s benchmarking survey, wages take up 19.2 per cent of the average pharmacy’s revenue and last year cost pharmacies nearly $15,000 more than in 2019 on average, due to increases to the minimum wage and pharmacies adding extra services.

It is hard to attract and retain a professional workforce because owners cannot afford to pay them well, Mr Gaudin says.

The Guide for Pharmacist Salary Banding, published by the Pharmaceutical Society in late 2017, recommends dispensing pharmacists should be paid $65,000 to $75,000 per annum (between $33.33 and $38.46 per hour).

But recent surveys of the profession show this target is often not met. In 2020, the Independent Pharmacists’ Association of New Zealand found 80 per cent of survey respondents earn between $32 and $45 an hour, although the hourly rate varied from $28 to $60 across the board.

But while about 90 per cent of all respondents earned $32.50 or more, about 10 per cent of pharmacists with more than 30 years’ experience earn no more than $35 per hour.

“We are losing pay parity relative to other health professions, we are seeing wage erosion and stress and burnout,” Mr Gaudin says.

He believes the diverse and responsive network of locally owned pharmacies offering quality services is in “real danger”.

There may be some light at the end of the tunnel. Mr Gaudin says DHBs are well aware of pharmacy’s viability issues and have committed to addressing them.

Last year, during talks on the National Annual Agreement Review (NAAR) of the contract, DHBs agreed to two independent reviews – of the wage cost pressures faced by pharmacy and the wider funding model.

Mr Gaudin says the first stages of these reviews went ahead last year and the findings, which are confidential, are with the NAAR for consideration.

The two reviews quantify the unmet cost pressures in pharmacy and determine how much extra funding is needed to cover them. The next stages are redesigning the pharmacy service and then working out a new funding and pricing model.

The new funding model informed by the review is due to be implemented by 1 October 2022, Mr Gaudin says.

He believes the model will need new money from Vote Health included in Budget 2022.

“We’re not going to have the money in time for Budget 2021.”

In addition to the reviews, the guild is lobbying health minister Andrew Little to remove the $5 prescription copayment.

Successive governments have refused to do this and following last year’s general election, Mr Little told Pharmacy Today he was aware of the copayment issue but had no plans to take action on it.

Last month, Pharmacy Today asked Ministry of Health chief pharmacy advisor Andi Shirtcliffe if anything has changed on the copayment.

Ms Shirtcliffe says pharmacy sector leaders have made sure the minister and ministry are well aware of the issue. In addition, the upcoming implementation of the Health and Disability System Review creates an opportunity to look at the issue.

However, before anything can change the Government needs to form a view on it – not just the Ministry of Health, also Treasury.

“I think we can all agree the copayment system isn’t perfect,” Ms Shirtcliffe says. “It is a government policy, it’s not just a health policy.”

When asked if the ministry was concerned about the viability of the pharmacy sector, Ms Shirtcliffe said the ministry regards core pharmacy services as an essential part of the health system, but most pharmacy funding comes from the ICPSA to which the ministry is not a party.

“I don’t want that to sound like we aren’t interested and its nothing to do with us. We do actually – myself and [pharmacy manager] Billy Allan and [group manager primary health care system improvement and innovation] Monique Burrows – sit around that contract table,” she says, adding they bring issues such as equity and ministry policy direction into the discussion.

“From a ministry perspective, we’re interested in safe, equitable and sustainable pharmacy and pharmacist services and that’s where our policy thinking and strategic thinking sits.”

In 2018, when the new pharmacy services contract came into force, former lead DHB general manager for pharmacy planning and funding Carolyn Gullery said pharmacy numbers were expected to “consolidate” under the new contract, and pointed out the DHBs had identified around 150 pharmacies that were essential and needed to stay open.

High numbers of pharmacies, particularly in Auckland, where there are 8.82 pharmacists per 10,000 people (the second highest concentration in New Zealand) have been identified as another possible cause of reduced viability as too many pharmacies are competing for funding.

Ms Shirtcliffe says the ministry has no policy as to what an acceptable number of pharmacy closures would be, and while she was not immediately familiar with the number of pharmacies, the last time she considered the issue, there was no crisis.

I think we can all agree the copayment system isn’t perfect... [but] it is a government policy, it’s not just a health policy

The ministry does not have a list of essential pharmacies that have to stay open to ensure services are provided, she says.

Exercises have been undertaken to

determine the approximate number of pharmacies required to maintain services in a disaster, but this is not intended for use during normal times.

“You might imagine you have four pharmacies down the high street and if, for whatever reason three of them shut their doors, the remaining one is going to be pretty essential.”

The Medicines Act means Medsafe has no powers to control pharmacy numbers. If a pharmacist applies for a licence and meets the criteria it must be granted.

However, Ms Shirtcliffe says the new Therapeutic Products Bill might give the ministry more flexibility with this type of regulation.

Dr Lee believes relying on funding from DHBs or the Government is not the only way to make pharmacies more viable.

The pharmacy services contract largely forbids pharmacies from passing any of the increased costs on to customers, which is what businesses in other sectors do.

She believes a user-pays model, where pharmacy is permitted to pass on costs to customers, would solve a lot of the current sustainability issues and the Government should take steps towards slowly introducing this.

“Realistically, the New Zealand Government cannot sustain a state-funded model forever. We have an ageing population which is larger than the next generation of taxpayers. And medicines and treatments are getting more expensive and complex.

“It can’t be free forever.”

Reading this feature might have filled you with doom and gloom, but there are still ways to turn things around even if nothing changes in the sector.

Retail consultant John Saywell believes pharmacies can become much more sophisticated in sales techniques and tactics.

“But I want to reiterate there is still an opportunity to do better with the value of each customer by increasing staff skill level and retail best practice.”

Many other retailers are gathering customer details and then targeting them with marketing later.

The closest thing pharmacy has to this is Green Cross Health’s Living Rewards card and even this is nowhere near the sophistication of other initiatives such as the One Card offered by Countdown supermarkets.

Even small retailers can do this sort of marketing, there are many affordable tools available these days, Mr Saywell says.

In addition, pharmacies should curate retail stock to focus on best-selling products, engaging in scientific store layout and range management, and using more sophisticated visual merchandising and marketing.

Pharmacies should also always be looking out for new categories entering pharmacy that are too technical or require too much advice to be sold by other retailers. For instance, sport support, wound care and compression stockings.

Auckland pharmacy owner HeeSeung Lee, who teaches a pharmacy leadership and management course at the University of Otago, also has some ideas.

One way is to make money out of services, either publicly funded or at cost to the consumer.

But before a pharmacy owner goes down this route it is important to do a thorough cost-benefit analysis to ensure income from the new service will cover the costs of offering it.

Immunisation is an area where pharmacies can still make a profit and Dr Lee is looking to expand into this in her own businesses.

Pharmacists are also able to charge for weight management, smoking cessation and sexual health services and Dr Lee believes it is possible to carve out a niche in these areas.

When times are tough, Dr Lee says it is essential to be open and honest with staff about problems and get their assistance in solving issues. Talk to them about reducing hours if necessary.

“These are very difficult topics to talk about, but if you are open and honest with staff they will be more sympathetic.”

You must also control your major costs (rent, wages and stock purchases) and cut everything else and talk to the bank early if you are having trouble, she says.

Make dispensing more efficient, with PACTs, robots, a good ordering system and electronic prescribing but be aware technology costs more than just buying the machine upfront, there is maintenance, stationery, etc, for using and the cost of training staff, she says.

Employing a business consultant can also help.

“Although it appears costly it may eventually save money.”

Finally, Dr Lee recommends every business owner reads the book

Profits First by Mike Michalowicz.

Academic pharmacist Nataly Martini highlights the importance of understanding non-Hodgkin lymphoma and pharmacists’ roles in managing this condition

Talking about butt stuff in the pharmacy can be awkward. Care Pharmaceuticals and Rectogesic® can help you get to the bottom of the issue